Inflation, Interest Rates and Housing

- theangryactuary

- Sep 12, 2023

- 4 min read

This holy trinity is front and center in the news right now. So it’s time to talk about what makes me angry when it comes to the way people look at housing. Housing is one of the three things that are essential to human life (food/water and clothing being the others). But like any of the essentials for life, it is debatable if any are a god given entitlement. Science and technology have made our modern lives so livable that many now believe these things to be a right and forget that any living being actually needs to make some sort of contribution to the world in order to receive the essentials of life. This is especially so for human beings as we can’t remain babies our entire lives, whether we suckle from our parents or wider society.

Housing:

There are many who believe that owning one’s own home is not just a necessity but also a right. That there should always be affordable housing to purchase at all levels of society. Although I’d agree that there needs to be government policy that provides for the timely construction of housing to allow a free market economy to balance supply and demand, it doesn’t mean that everyone needs to own a roof over their heads.

At the end of the day, a house is like any other good. Like cars, there are varying levels of size, cost and amenities. Being very economically rational minded, it is up to each individual to look at what is affordable and make a purchase accordingly. Just because I want a Ferrari doesn’t mean I take on debt to buy it when I clearly can’t afford it. “But what if one can’t afford any house?” Guess what? It’s called renting. I would argue that there is nothing wrong with renting for one’s entire life. You can’t take a house with you to the afterlife. A home is meant to provide shelter while we are alive. Like any other good it is useless to us once we have passed.

“But I want to pass on my home to my offspring.” There’s nothing wrong with passing on a home or any other asset, but a home for most people seems to be more of a place to store our shit than anything else. Clutter is real, just ask Marie Kondo. I’d argue that any un/grateful offspring would prefer something more liquid, like cash, stocks or bonds. This also puts us on the slippery slope to discussing inheritance in general, but I’ll save that bug bear for a different day.

Finally, we keep hearing about people treating their home as an investment. They argue that they feel wealthier knowing that the home they live in has gone up in price. This gives a false sense of wealth and actually leads people to spend more on discretionary items (like any other source, feel free to google it). Unlike other assets, a house we live in is not easily sold and leaves us the problem of having to find somewhere else to store our shit. Again, look to Marie Kondo here. The chances are, if your house price has gone up by 20%, so have the properties around you, so if you wanted to change homes, you wouldn’t be better off.

Interest rates:

For the vast majority, owning a home includes the fun activity of taking on a mortgage. There’s nothing like borrowing money to own the rights to your dream home. For the 90% of Americans who are fortunate enough to have 30 year fixed mortgages, hats off to you. If you refinanced before Covid, you’re doing well. You’ve likely locked in debt that will cost you much less in interest than recent inflation rates.

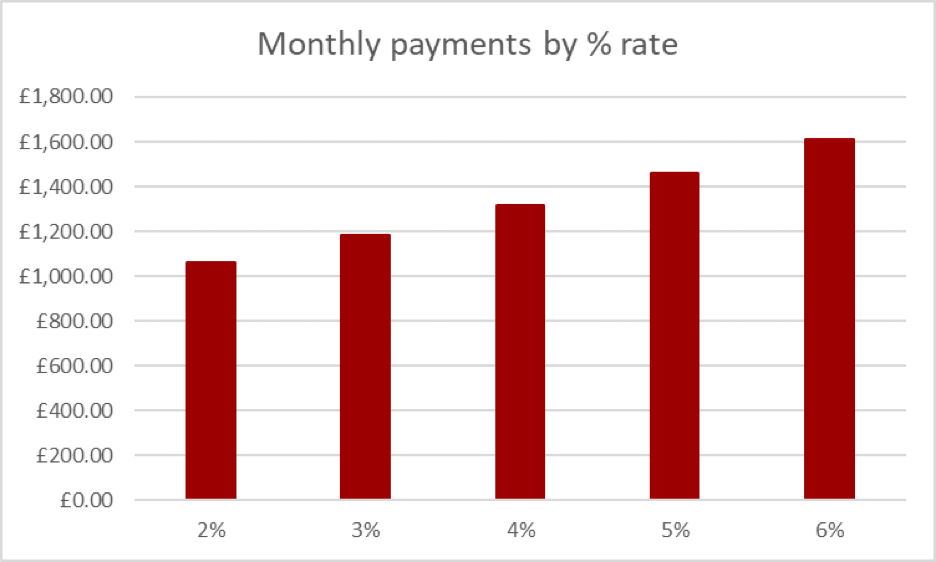

For the rest of the world (like in the UK), mortgages are only fixed for a 2-5 year period before reverting to a floating rate. At the end of the fixed period, a new fixed period can be started, however, this would be subject to the new interest rates at the time. For many, this refinancing is absolutely killing the household budget. For a loan of £250,000 over a 25 year term, the difference in monthly payments payments between a 2% interest rate and a 6% rate is over £500 a month. When the original monthly payment at 2% was around £1050, this is an over 50% increase in monthly payments from a 4% increase in interest rates. Compounding can certainly be a pain in the a$$.

The increase in interest rates is caused by the central bank increasing the base rate that commercial and retail banks can borrow at. This rate then flows onto people like you and me when it comes to mortgages. Increased rates makes buying a home less affordable. When this is unaffordable for more people, it causes downward pressure on house prices. But why did the bank need to increase the interest rate in the first place?

Inflation:

So what caused these crazy interest rates? Well, modern economic theory tells us that when we have high inflation, it means that the cost of goods is increasing faster than we can afford to match in terms of our earnings.

Turkey is a great example of what happens when you ignore inflation and throw the playbook out the window. Turkey recently had a huge bout of double digit inflation, rising to above 75% at the height in 2022. Multiple central bankers appointed by the president where ignored. Conventional theory recommends a raising of the central bank rates to counter inflation. But Turkey decided to do the opposite and also lower interest rates. This had the effect of putting even more fuel on the fire, resulting in an upward spiral for prices.

When inflation rises, it is because there is too much money in the system chasing too few goods, causing prices to rise. This can be true not just of goods but also of labour. When rates increase, this makes borrowing to purchase goods more expensive, thereby decreasing demand. This in turn better balances supply and demand, reducing the pressure on prices to increase. There are, of course, implications to the wider economy but that is for another time.

At the end of the day, inflation and interest rates will have fluctuations over the life of a 20+ year mortgage. That’s why it is important to purchase a house that is affordable in case there are unfavourable fluctuations. Owning a house is a privilege and not an automatic right. Buy wisely or rent and use any savings to build an investment pot for the future.

Further reading:

Comments